Virtual cards have long been the preferred choice for ad account payments. They’re easy to set up, straightforward to use, and accepted by major platforms like Meta, Google, LinkedIn, and more. However, many financial providers now offer cards specifically designed for each platform. For example, you can get a card just for Facebook Ads or one for Google Ads. But what if you want a single card that covers all your ad expenses? This guide will show you how to choose the right card for that purpose.

Choosing a universal card for ad payments: key features

Opening a single virtual card can be a smart move. With a universal card, you can segment your ad spend by campaign rather than by platform, which can be convenient if you’re running a 360-degree campaign. With one virtual card, you can cover all expenses across Facebook Ads, Google Ads, LinkedIn Ads, Instagram Ads, and more. This setup makes it easier to control and analyze your spending.

Most major ad platforms have similar requirements. First, most platforms support payments via Visa and Mastercard. Second, they prefer banks with a solid reputation from the U.S., the EU, or the UK. Third, payments are typically made in USD or EUR.

Additionally, a universal card for ad payments should cover all your ad costs. This means it should have a high spending limit and low transaction fees. High limits are easily achieved by opting for credit cards, which are often more accepted by ad platforms.

Based on these factors, we’ve chosen the top five virtual card providers for ad expenses on any platform. Our selection includes both high-limit debit and credit cards.

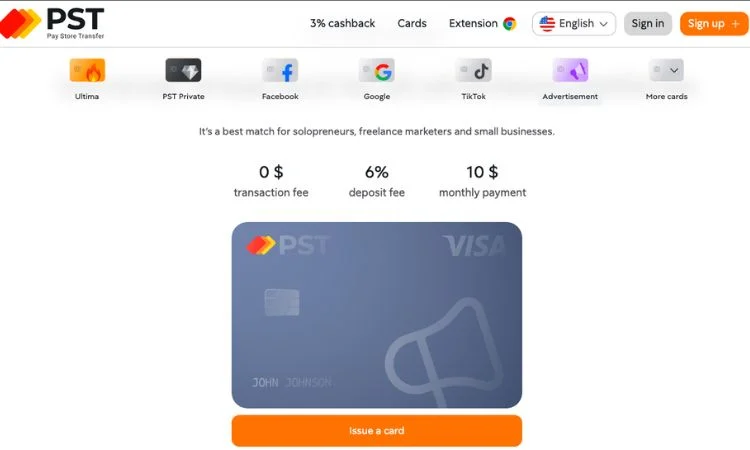

1. PSTNET

PSTNET offers Visa and Mastercard digital cards with trusted BINs from U.S. and European banks. Users can open segmented cards for each platform or choose a universal debit or credit card. All cards have unlimited spending, zero transaction fees, and no additional charges for withdrawals or declines.

PSTNET’s virtual cards are often rated the best credit cards for ads, thanks to a 3% cashback on spending. To open a card, users must join the PST Private program, which allows them to issue an unlimited number of cards. This program is ideal for agencies managing multiple campaigns, as it offers up to 100 free cards per month, with card costs depending on the chosen plan.

Features:

- Team Collaboration Tools: Assign tasks, set roles, and establish card limits for team members.

- Free BIN Checker: Access a database of over 500,000 BINs, updated daily.

- Spending Analytics: Provides users with detailed financial reports.

- Crypto Card Funding: Supports BTC, USDT (TRC20, ERC20), and 16 other cryptocurrencies.

- Standard Card Funding Methods: SWIFT/SEPA bank transfers, Visa/Mastercard cards.

- Registration: Use Apple ID, Google account, Telegram, WhatsApp, or email.

- Support Service: 24/7 Available via Telegram, WhatsApp, or live chat.

- Telegram Bot: Get 3D Secure codes and service updates via bot notifications.

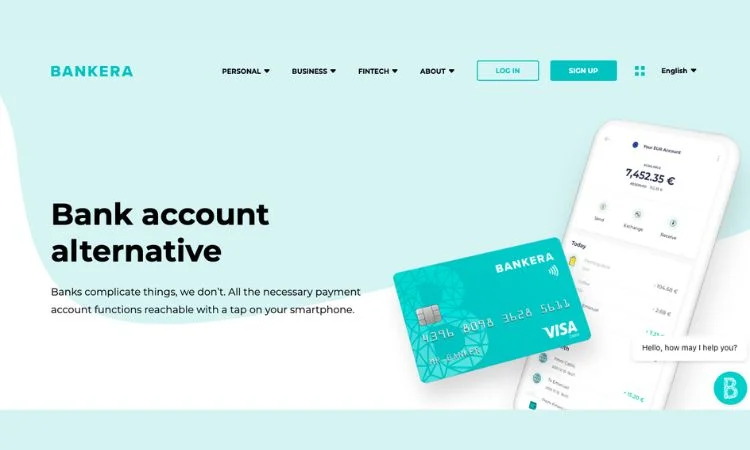

2. Bankera

Bankera is a Lithuanian-accredited financial solution offering both digital and physical cards for business needs. Its main features include multi-currency accounts and cryptocurrency support.

Bankera’s virtual cards, based on Visa, support transactions in USD, EUR, and GBP. The service’s debit cards have high spending limits, allowing daily transactions up to 100,000 EUR or 300,000 EUR per month. Each transaction has a limit of 50,000 EUR.

Bankera also has a fee structure, with account setup starting at 450 EUR for non-EU/UK companies and monthly maintenance fees up to 200 EUR for cryptocurrency accounts (50 EUR for non-crypto accounts).

Features:

- Team Collaboration Tools: Not provided.

- Spending Analytics: Reports can be requested from the service manager or tracked via the user dashboard or app.

- Crypto Card Funding: Supports USDT (TRC20, ERC20) and other coins through SpectroCoin.

- Standard Card Funding Methods: SEPA/SWIFT bank transfers, Visa/Mastercard cards.

- Registration: Takes 10–15 days due to multi-step verification.

- Support Service: Available via live chat and email.

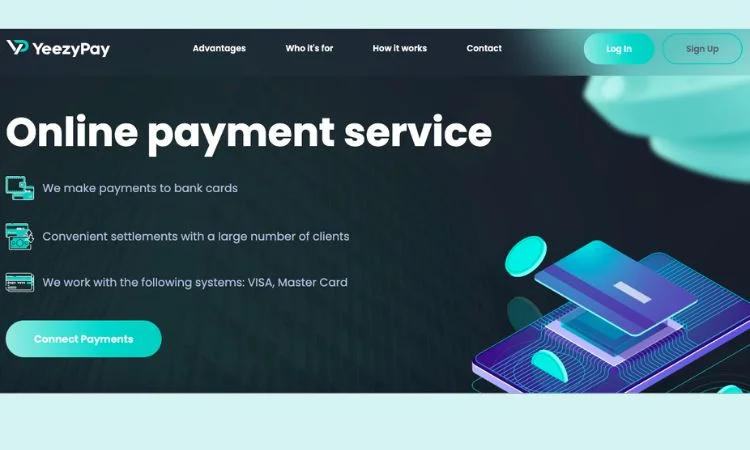

3. Yeezypay

Yeezypay’s virtual cards are available in minutes and are issued on Visa, Mastercard, and UnionPay networks. Cards can be funded with USDT (TRC20), and payments can be made in USD or EUR with no transaction limits.

The issuing banks are located in the U.S. and EU, with seven BIN options available to users. There are no transaction or decline fees, but each card requires a minimum deposit of 107 USDT.

Features:

- Team Collaboration Tools: Not provided.

- Spending Analytics: Available via the service manager through Telegram.

- Crypto Card Funding: Supports USDT (TRC20).

- Standard Card Funding Methods: Not available.

- Registration: Through a Telegram bot, takes less than a minute.

- Support Service: Available via Telegram.

4. Spendge

Spendge specializes in cards exclusively for ad account payments, offering both segmented and universal credit cards. Spendge’s cards work on Visa and Mastercard, with no spending or quantity limits, and BINs from banks in the UK, Bulgaria, and Ireland. The platform also supports crypto invoicing.

Users can issue cards in slots, with a test option (Custom Quantity), and plans for 30 and 100 cards. Transaction fees are 1% + $0.30, with decline fees varying by card BIN.

Features:

- Team Collaboration Tools: Role assignment.

- Spending Analytics: All transactions are reflected in dashboard statistics.

- Crypto Card Funding: Supports USDT (TRC20).

- Standard Card Funding Methods: WIRE bank transfers.

- Registration: Requires account verification, with status updates shown in the dashboard.

- Support Service: Weekdays 9:00–18:00 (GMT+3).

4. EPN

EPN’s virtual cards are designed for any online payments, including ad costs. All cards work on Visa/Mastercard networks, issued by 36 banks in the U.S. and Europe, and support USD and EUR.

A minimum deposit of $30 is required, with no transaction fees or spending limits. However, experienced users recommend not linking EPN cards directly to ad accounts, as occasional restrictions can arise.

Features:

- Team Collaboration Tools: Role assignment and card management.

- Spending Analytics: All transactions are visible in the user dashboard.

- Crypto Card Funding: Supports popular cryptocurrencies.

- Standard Card Funding Methods: SWIFT bank transfers, Visa/Mastercard cards.

- Registration: Via Google account or email.

- Support Service: 24/7 support through Telegram or ticket system on the website.

Conclusion

Virtual cards are the optimal solution when you need a versatile payment tool for marketing campaigns. When choosing a card, look for one that supports multiple currencies, works with major payment networks, and offers sufficient spending limits. Prioritize cards issued by banks in the U.S., the EU, or the UK.

In this guide, we reviewed PSTNET, Bankera, Yeezypay, Spendge, and EPN. The digital cards from these providers can be used across all major ad platforms, from Facebook Ads and Google Ads to LinkedIn Ads.

PSTNET

- Payment Networks: Visa/Mastercard

- Supported Currencies: USD, EUR

- Limits: None

- Transaction Fees: 0%

- Decline Fees: 0%

- Issuing Banks: US, EU

- Number of BINs: 25+

Bankera

- Payment Networks: Visa

- Supported Currencies: USD, EUR, GBP

- Limits: €300,000 per month, €50,000 per transaction

- Transaction Fees: 0%

- Decline Fees: Varies by user terms

- Issuing Banks: EU

- Number of BINs: 8

Yeezypay

- Payment Networks: Visa, Mastercard, UnionPay

- Supported Currencies: USD, EUR

- Limits: None

- Transaction Fees: 0%

- Decline Fees: 0%

- Issuing Banks: EU, US

- Number of BINs: 7

Spendge

- Payment Networks: Visa/Mastercard

- Supported Currencies: USD, EUR

- Limits: None

- Transaction Fees: 1% + $0.30

- Decline Fees: Varies by card BIN

- Issuing Banks: UK, EU

- Number of BINs: 6

EPN

- Payment Networks: Visa/Mastercard

- Supported Currencies: USD, EUR

- Limits: None

- Transaction Fees: 0%

- Decline Fees: Varies by user-specific terms

- Issuing Banks: US, EU

- Number of BINs: 42

In ad payments, it’s essential to consider not only the payment tools but also any evolving security features and platform-specific requirements. Before launching any 360-marketing campaign, review platform policies to avoid declines, and, if necessary, quickly create a new card with no transaction history.